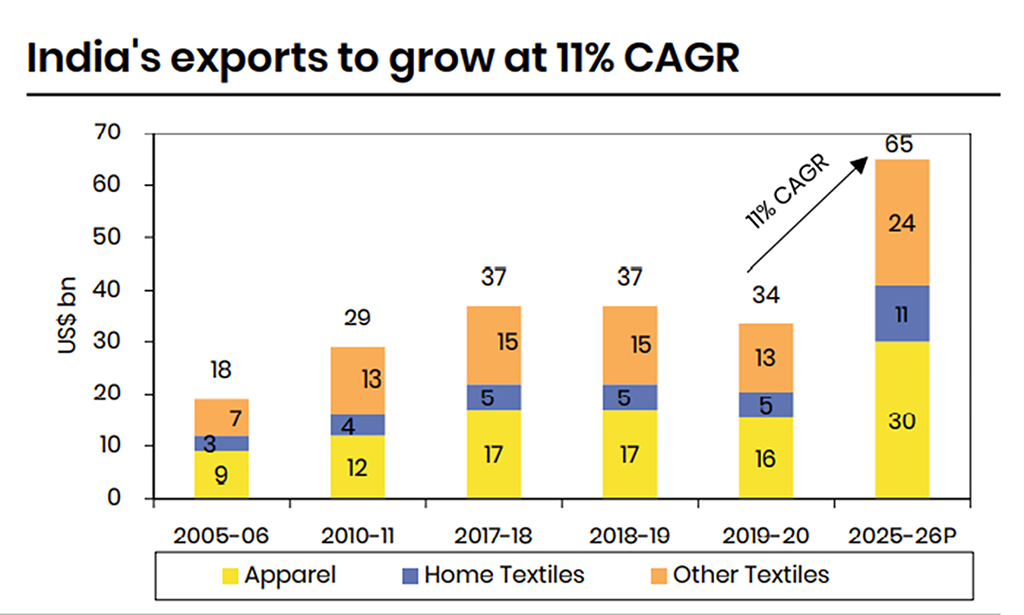

After a long wait the situation changed in favour for India in the global textile world. As per the report of Wazir Advisors the Indian textile industry worth USD 140 billion is expected to grow at 11% CAGR to reach size of USD 225 billion by year 2026. This growth is likely to come mainly from increased exports.

Factors favouring growth in exports

Growing global demand: Post pandemic, demand for home textiles and knitted apparel has gone up. Consumption increased due to hygiene consciousness and work from home culture.

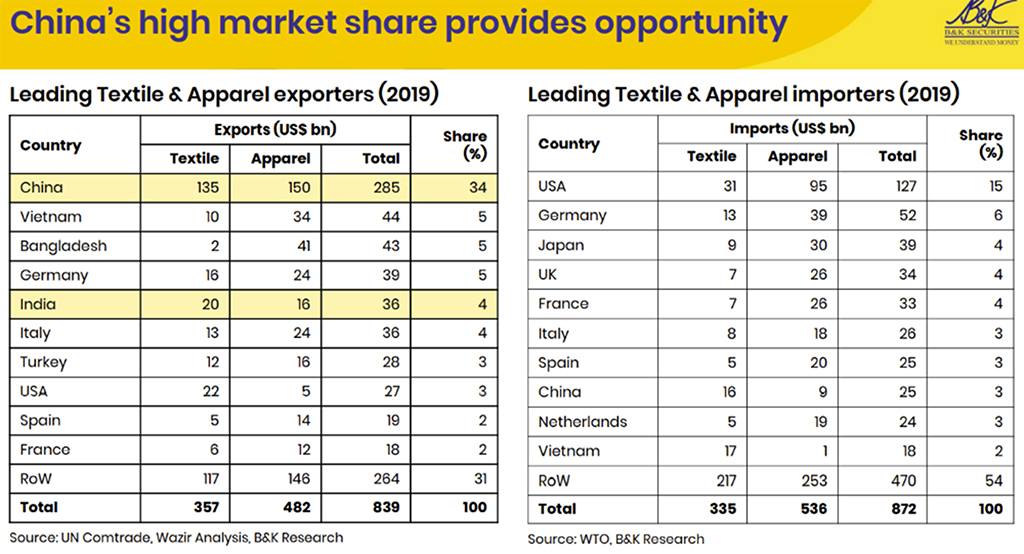

India’s competitive strength: India’s self-sufficiency in raw materials, presence across entire value chain and manufacturing capacity are the factors favouring India over other countries. Even 1% market share gain will provide India an opportunity of USD 8 billion in exports.

China+1 policy of buying houses: India is on the way to gain substantial market share in the global textile trade due to structural shift in the buying of the retail houses and brands. US and EU, forming nearly 34% of global textile and apparel imports, are looking forward to reduce dependence on China.

US ban on Xinjiang cotton: The ban on Xinjiang cotton (84% of China’s cotton production) by US will bode well for India as it is strong in cotton-based products. The space created by blocking of Chinese cotton products can be partly filled by India with its integrated textile value chain & availability of cheaper cotton.

Government support at its best: Government has announced many visionary schemes such as PLI, MITRA. These along with the extension of RoSCTL will help in increasing exports. Textile minister Mr Piyush Goyal has already announced ambitious targets for textile exports.

Weak INR to play in India’s favour: Indian Rupee has depreciated much more vis a vis Chinese RMB against USD. This factor will benefit Indian exporters in gaining market from the Chinese suppliers.

Factors posing hurdle in India’s export growth upcycle

Increasing cotton and yarn prices: Continuous increase in the raw material and yarn prices over the last couple of months have created a problem for the exporters. The yarn needs to be made available at reasonable prices to fabric makers to remain competitive in exports.

Failure to create large capacities in garments: China can offer larger volumes while India cannot due to scattered garment capacities. India needs to have large size manufacturing facilities in garmenting to come back in the game.

Non-adherence to quality standards and delivery: China has been successful in global trade due to its strong adherence to quality and also honouring the delivery. Indian suppliers need to give importance to consistent quality and fulfilling of shipment commitments.

Delay in closing FTAs with importing countries: Indian exporters are at disadvantage to due discriminating duty treatment vis a vis Turkey, Vietnam, Sri Lanka, Bangladesh, Pakistan and Cambodia in the EU and UK markets. If India fails to close FTAs with EU, UK, Canada and Australia in the near future, it is likely to lose the market opportunity.

Losing cost-competitiveness: The lower labour cost is an advantage at present but in case of any increase, the competitive edge will be lost to Bangladesh and Vietnam. Indian labour productivity is also lower compared to other countries which also adds up to cost inefficiency.

Need to go after so far untapped opportunities

There are some global market opportunities which India has failed to encash due to many reasons.

Japan market: India has 1.5% share in apparel imports of Japan. The Japanese buyers demand stringent quality, due to which Indian exporters prefer to turn their back to Japan. India can’t afford to neglect big market like Japan.

Manmade fibre-based products: India has been traditionally strong in cotton while majority of the global textile trade is in manmade fibres. Indian exporters so far missed opportunities in the global trade due to this reason. There are larger opportunities for grab in knit goods, activewear, functional fabrics and technical textiles.

Global apparel trade: More than 55% of the global textile trade happens in apparel where India is weak. Since China is vacating space in apparel trade, sizeable opportunity is open for India. Big corporates should invest in creating larger capacities in garmenting.

Brand India: Indian textiles are mainly occupying lower value segments in the global markets due to lack of quality and consistency. Need is to build ‘Brand India’ in the international markets. This can open up opportunities in high value textile products.

Technical Textiles: With help of the PLI scheme for technical textiles, India can create surplus capacities in technical textiles for exports. Hygiene products, industrial textiles and automotive textiles have large scope for exports.

Challenges in the way forward

Although India appears to be in an advantageous situation in the global trade there are some serious challenges which Indian textile manufacturers will face.

Sustainability and Environmental issues: The textile industry is one of the most polluting industries. Demand for sustainable products will be on rise. Industry needs to focus on environmental compliance. Indian manufacturers have to invest in new technologies which can save energy, generate less waste and save environment.

Quality-oriented ecosystem: Indian manufacturers lack stringent quality infrastructure and the ecosystem. World demands consistent quality. Serious efforts are required to inculcate ‘zero defect’ and ‘do it right the first time’ manufacturing culture.

Skill development: Skill deficit leads to lower productivity and quality issues. The Textile Skill Council is helping in this but it will take long for Indian labour to adopt global manufacturing culture. Skills will be very crucial in maintaining India’s competitiveness.

Scarcity of resources and rising input costs: Water will be in scarcity with the ever-increasing demand for drinking water due to increasing population. Recycling and Reuse will be the key. The rising costs of raw materials, labour and other input materials will lead to risk of India losing competitive edge.

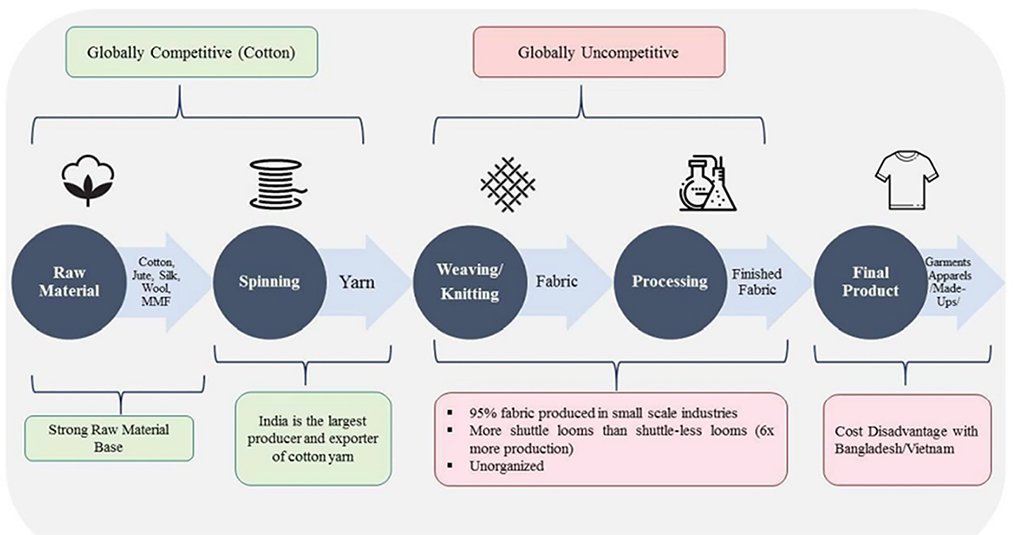

Imbalance in the textile value chain: Spinning is fairly modern resulting in India’s strong position in yarn. However, weaving and processing sectors have deficit in modernisation. 70% of woven fabric production comes from power loom sector while large portion of processing is done in decentralized sector. This can become a main hurdle in increasing exports as well as moving up the value chain.

Conclusion

India is certainly in a sweet spot with many factors favouring structural shift towards India. For the newly created space by China in global trade, India can find itself in the front pole position. However, for gaining global share, India needs to diversify its product basket with many man-made fibre-based products, create world class capacities in garmenting, adopt automation and digitization for efficient manufacturing, inculcate stringent quality culture, improve the infrastructure, focus on sustainability and above all create trust in the minds of buyers. With these factors in place, nobody can stop the juggernaut of the Indian textile industry.

10% market share in the global textile trade (from the present 5%) might appear ambitious. The challenges and hurdles are many but if all the textile value chain constituents align and work as one team supported by the government, India will not be far from securing its due place in the global textile trade. For the Indian textile industry, the past was challenging while the present is good but the best is waiting to come in the near future.