By Sanjay Arora, Wazir Advisors (sanjay@wazir.in)

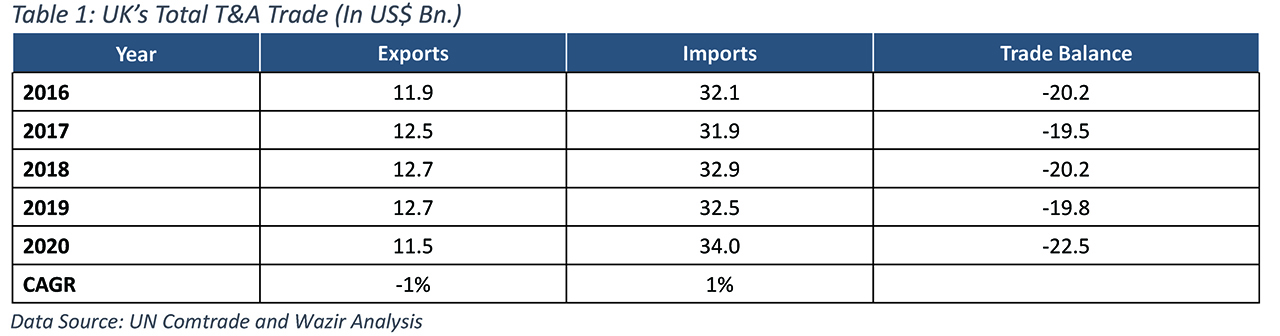

United Kingdom is one of the largest market for Textile & Apparel (T&A) in the world. British consumers spend on an average US$ 80 bn. on fashion and textiles every year. Aside from being a global Market, it also performs a considerable amount of manufacturing, with approx. 105,000 people directly employed in the manufacturing industry. In year 2020, the country’s T&A imports stood at US$ 34 bn. growing at a CAGR of 1% since 2016 whereas, the exports registered US$ 11.5 bn. in value declining at a CAGR of 1% during the same period making UK’s T&A Trade balance a deficit of US$ -4.4 billion on average.

Brexit: UK’s T&A Industry to experience some difficulties till the transition takes place.

On 31 January 2020, after over 45 years of membership, UK formally left the EU leaving a far reaching effect on its fashion industry. As more than 70% of UK’s T&A export goes to the EU, the industry is seriously concerned about the possibility that the agreement might jeopardize its trade relations with the EU. Moreover, UK’s T&A industry is dominated by SMEs and micro businesses with 82% of companies employing fewer than 10 people, which makes it difficult for many fashion companies to adapt to the new UK-EU trade agreement, as it involves higher trade costs in the form of non-tariff barriers such as customs procedures, documentation requirements, and regulatory compliance. There is also a growing concern over the impact of the agreement on the employment pool available to the industry, as a large workforce employed under the T&A industry comes from The EU. For suppliers exporting to UK, the nation had already agreed to provide duty-free market access to the country under the EU’s Generalized Scheme of Preferences (GSP), namely the Everything but Arms (EBA) arrangement, to 48 LDCs. However, on the export front, the country is rapidly working on forging new trade policies with its key export markets such as USA, Japan, China, Australia Canada and New Zealand. Overall, UK officials ensured that difficulties being faced by UK’s T&A are temporary and will vanish once the transitions is settled.

UK’s T&A – Import Scenario:

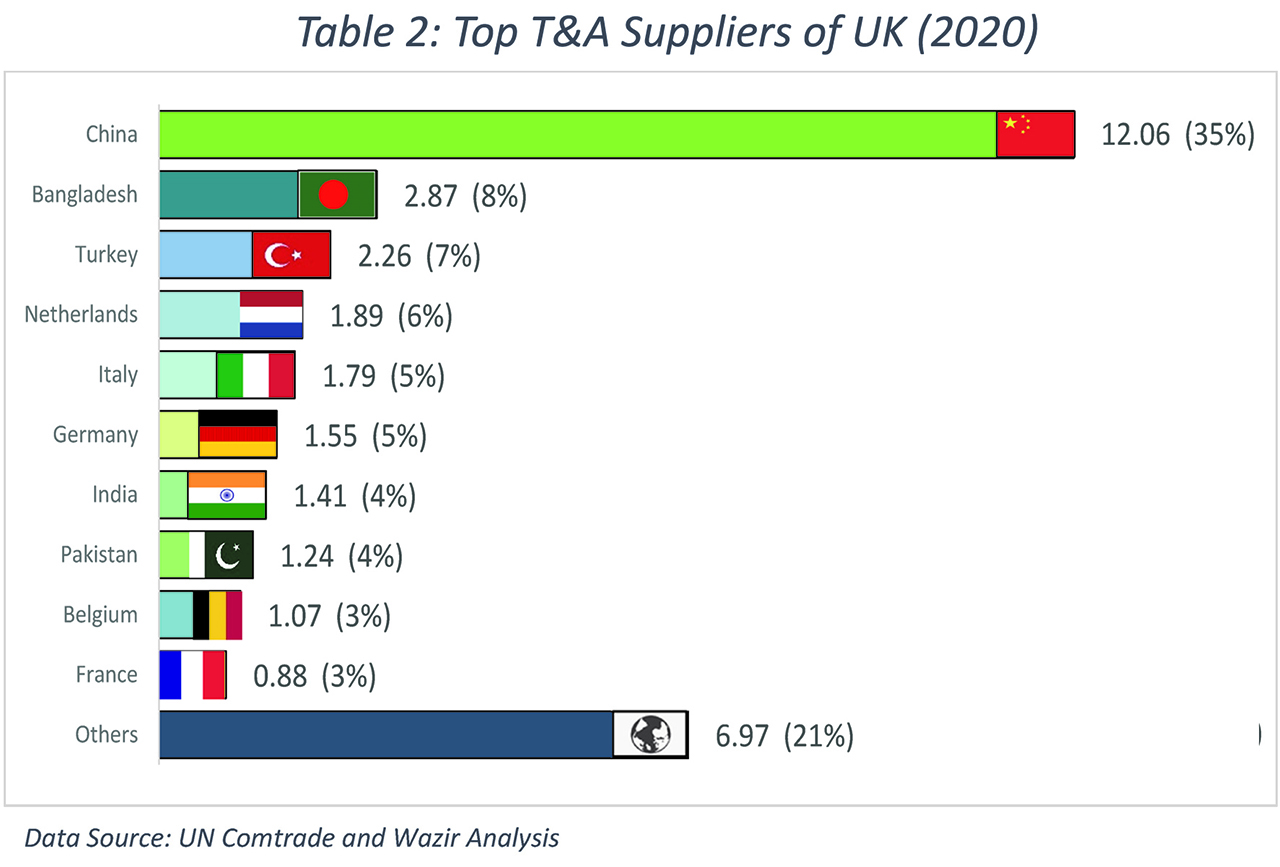

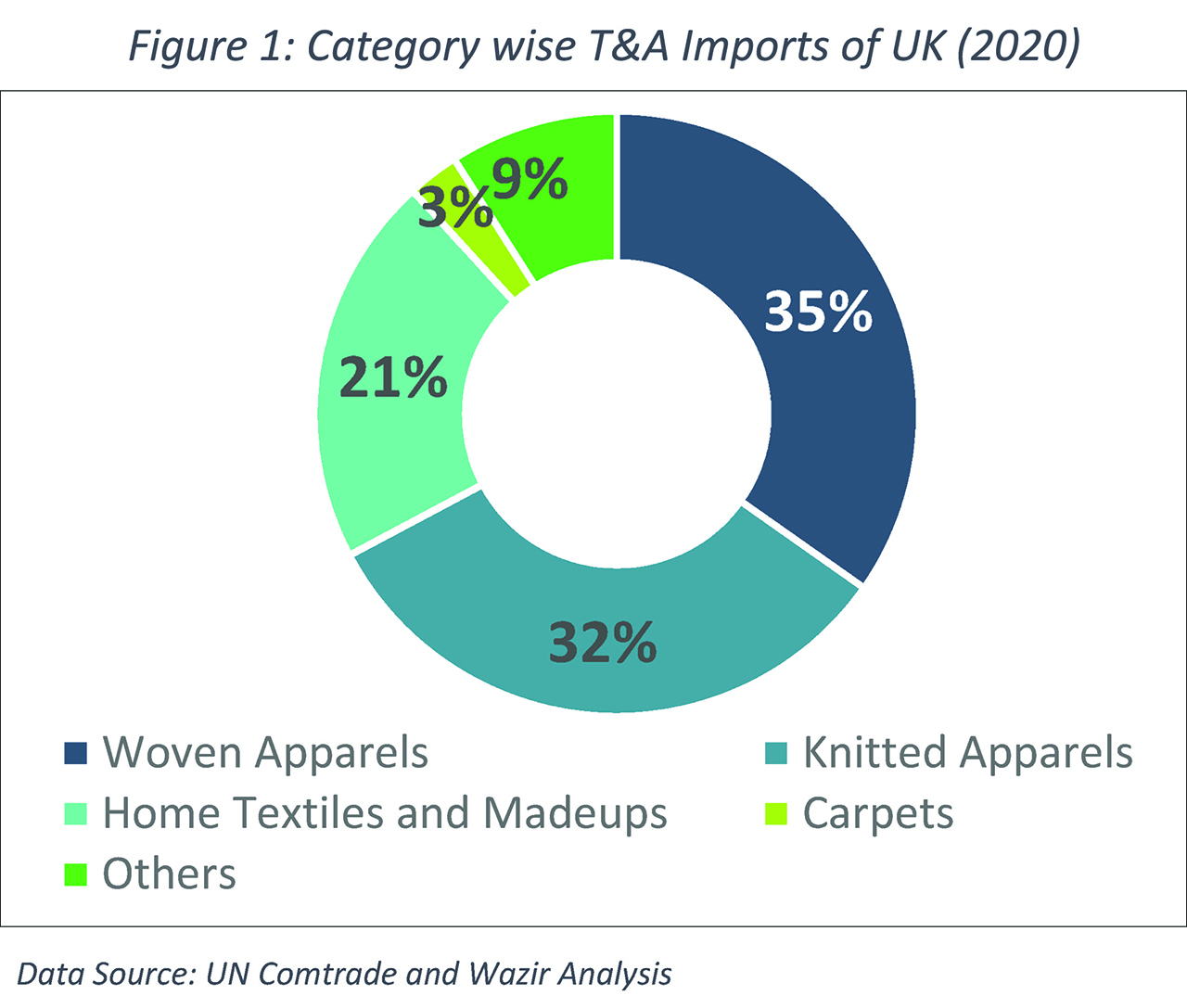

UK’s imports of textile and apparel stood at US$ 34 bn. in 2020. The country’s imports increased by 5% over last year despite the ongoing crisis. However, the growth is majorly due to the imports of coveralls, masks and PPE kits. In, 2020, country’s home textile & made-up segment, (which includes PPE kits and mask as well) experienced a drastic increase of 173% and stood at US$ 7.1 bn. against US$ 2.6 bn. of last year. Overall, the market is dominated by Knitted apparels, followed by woven apparel with 35% and 32% share, respectively. The top 4 exporters of T&A to UK are China, Bangladesh, Turkey and Netherlands, together they account for around 56% of the T&A imports to the country.

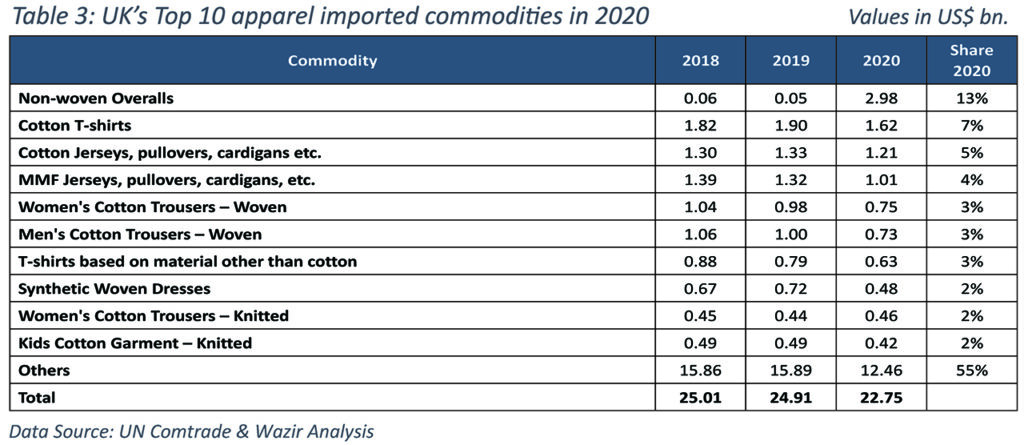

The maximum share in imported apparel commodities comes from Women’s apparel which is almost double of Men’s apparel. Woven Women’s suits and ensembles was the largest imported category in 2020 with a share of 14% followed by Jerseys and Nonwoven Coveralls with a share of 12% each. T-shits, Women’s Knitted suits, Men’s knitted/woven suits and blouses were also among the top 10 imported commodities of 2020.

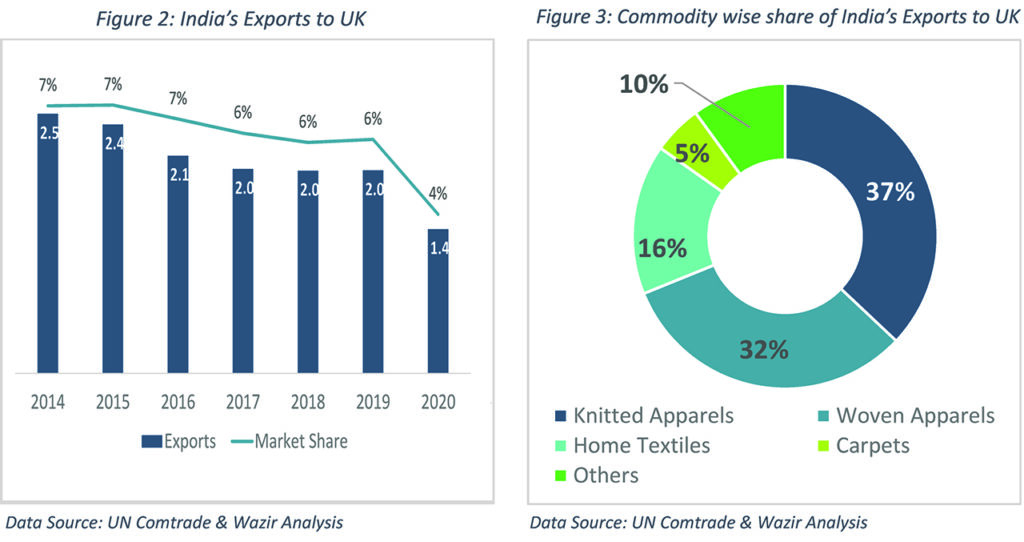

India’s Textile and Apparel exports to UK: India working to sign a Free Trade Agreement (FTA) with UK

For India, the UK is the third largest market for Textile and Apparel (after USA and UAE, respectively). India’s exports to UK stood at US$ 1.4 bn. in 2020, down from US$ 2 bn. in 2019. However, barring 2020, India’s share in UK’s T&A imports has remained steady around 6%. Among the T&A commodities imported from India, Apparels holds the majority share of around 70% followed by Home Textile and Made-ups – 16% (which include PPE kits and Masks).

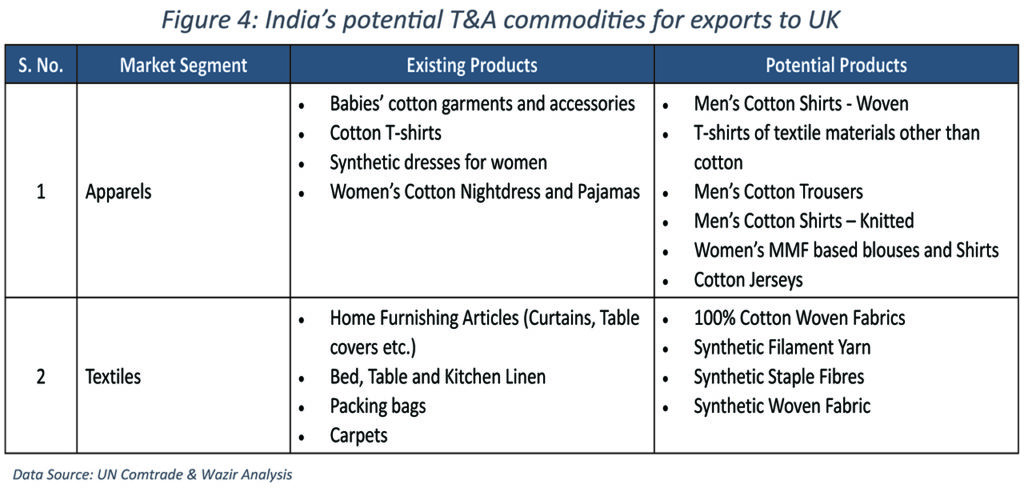

There is a huge market opportunity for India to capitalize in UK’s T&A market. Commodities such as cotton shirts, t-shirts, cotton trousers, women’s MMF based blouses and cotton jerseys are among the top categories in UK’s market in which India accounts just a marginal share. These commodities can be looked up as attractive categories from UK’s T&A market perspective. Also, on the textile front there are products such as cotton Woven Fabrics, Synthetic Filament Yarn, Synthetic Staple Fibre and Fabric which hold good potential considering the future outlook of the UK’s textile market.

While UK’s decision of continuing to grant preferential trade benefits to 47 Least Developed Countries (LDCs) is expected to benefit Bangladesh, India on the other hand would be vulnerable to a higher import tariff. India currently enjoys a 20% duty relaxation on import duty to the EU, with Brexit this relaxation will not be available to India. However, India is hopefully of signing an independent FTA with UK soon. Additionally, the Textile Ministry of India has initiated discussion with UK’s policy makers for an early trade pact for apparel in the run-up to FTA. The pact will help India in strengthening its share in UK’s imports.

Wazir Advisors, your trusted business advisor in Textile and Apparel sector can assist you in strategy formulation and implementation, forming alliances and joint ventures, investments, market understanding, sector analysis and due diligence, thereby providing end-to-end solutions spanning the complete business cycle in textile value chain. Wazir can also help you in understanding and strategizing your business to align well with the British Textile and Apparel market.