India, the world’s largest democracy and one of the fastest growing economies, is an active hub for investors from all around the world. As per projections by the International Monetary Fund (IMF), India will soon overtake Germany as the world’s fourth largest economy. In recent times, India has attracted significant FDI and indigenous investments in 25 major sectors in line with the Government’s “Make in India” initiative. As per the FDI report 2018 by FDI Intelligence, India was ranked the second highest in terms of FDI by capital investment and first for job creation, with 161,445 jobs announced in 2017. India has also improved its World Bank Ease of Doing Business (EODB) ranking from 142 in 2015 to 77 in 2018, securing a place among the top 100 countries.

The booming textile and apparel (T&A) sector accounted for about 12 per cent of India’s total export earnings in 2017-18 and provides direct employment to 52 million people and indirect employment to 69 million people. It has the double advantage of being export-competitive as well as having a large and growing domestic market.

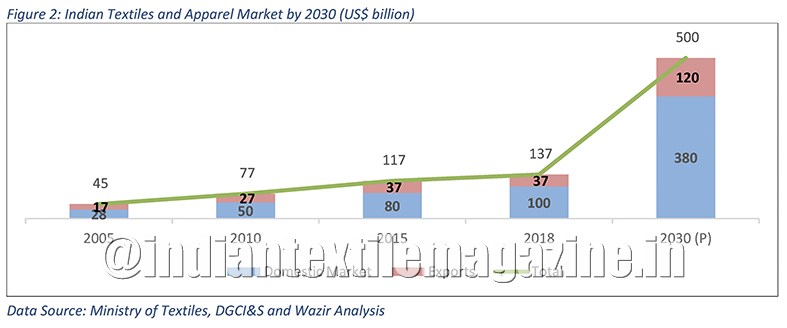

The T&A market in India was estimated at $137 billion in 2018. The domestic consumption of textiles and apparel is around $100 billion, constituting approximately 70 per cent of the total market size, while exports make up the rest 30 per cent with $37 billion.

Over the decades, a major part of textile and apparel manufacturing has moved from developed countries like the US, the EU and Japan to regions like China, South Asia and South-East Asia. Today’s textile and apparel sector is again at the cusp of major structural changes. China, a dominant player, is now seeing its share in global trade falling due to rapidly increasing domestic consumption and rising wages. An additional aspect is the so-called ‘trade war’ between the US and China wherein the former is expected to increase import duties on apparel made in China significantly. This is, in turn, creating trade opportunities for competing nations like India, Bangladesh, Vietnam and Ethiopia. India has the potential to benefit the most.

Organized retail in India currently stands at around 10 per cent of the overall retail market of $815 billion and, within this, apparel has a share of approximately 35 per cent. With changing consumer dynamics, a growth in disposable income, favourable demographics, changing lifestyles and a high potential for penetrating non-urban metro markets, the share of organized retail in India is expected to reach 14 per cent by 2030.

Looking at the macro-economic factors and emerging trends, we believe that the real growth phase of the Indian textile and apparel industry is yet to start. The industry has the potential to reach $500 billion by 2030.

India is poised to be the powerhouse for textile and apparel manufacturing, exports and consumption in the near future, and the following factors prove this to be true.

- India has had a stable and supportive Government which has been instrumental in forming business-friendly policies. As a result, foreign direct investment (FDI) inflows in India in 2017-18 amounted to $61.96 billion. India has emerged as one of the most attractive destinations for investment and business in recent years with a cumulative infusion of FDI worth $546 billion since the start of the 21st century. Prudent macro-economic policies have resulted in a consistent economic growth over the past years. The GDP growth is from 5.5 per cent in 2012 to 6.7 per cent in 2018, amounting to a massive $2,690 billion, as compared to the world GDP growth of 2.6 per cent in 2012 to a meagre 3.14 per cent in 2018.

- Also, India’s infrastructure sector has witnessed a remarkable growth in the last few years, with facilities coming up in various parts of the country. The Indian Government has an ambitious target of pumping $375 billion into developing infrastructure by 2020, including $120 billion for building 27 industrial clusters and an additional $75 billion for road, railway and port connectivity projects.

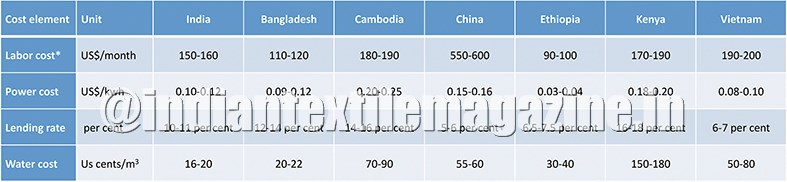

- Add to that the competitive cost of manufacturing that India offers, and you have the perfect mix of ingredients in this recipe for success. The wage cost in India is higher than in Bangladesh but lower than in China and Vietnam. In terms of power cost, India is comparable to low-cost destinations like Bangladesh, Vietnam, Myanmar and Kenya, etc., but higher than that in China. The lending rates in India are on the higher side as compared to China and Vietnam, but with the special Government support available for this sector, the effective cost of capital becomes comparable, as is evident from Table 1 below.

- Manufacturing in India, for India, is the way to go currently. In the last decade, the Indian domestic market has performed better than the largest consumption regions like the US, the EU and Japan. The domestic consumption of textile and apparel is already worth $100 billion as of 2018, and it is estimated that the market size will touch $380 billion by 2030. Also, studies show that countries, after achieving a per capita GDP of more than $2,500, experience a spur of economic growth led by consumer spending, which the Indian economy is expected to reach by 2021. This will help in an exponential growth of textile and apparel consumption in the country.

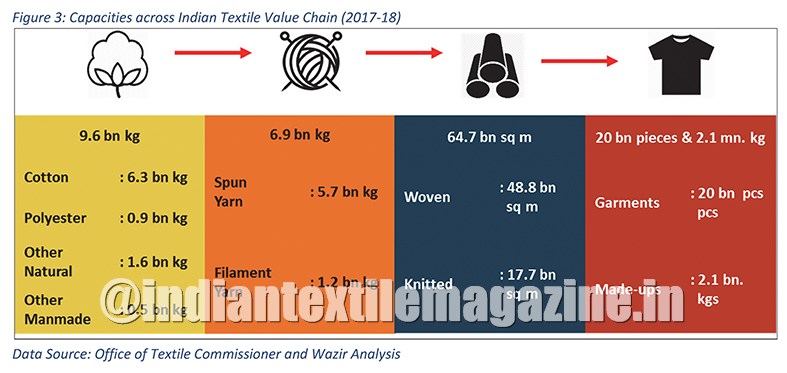

- Being an all-in-one manufacturing package also works in India’s favour. India is one of the few textile manufacturing countries in the world where all levels of textile value chain, i.e., from fiber/filament to garment/made-ups manufacturing, are present. In contrast, countries like Bangladesh, Vietnam, Sri Lanka, Myanmar, Ethiopia and Cambodia have fragmented value chains; most are focused on end-products and are dependent on other countries for fabric and yarn. India’s huge capacities across the textile value chain offer raw material security and hence reduced costs for production. This also provides flexibility to stakeholders to diversify into any segment of the value chain, depending on the market demand and profitability.

- There is abundant availability of ready-made infrastructure for the textile and apparel industry, including the Textile Parks developed under the Scheme for Integrated Textile Parks (SITP) which was launched in 2005. Under the scheme, the Government assists the park developers by providing 40 per cent of the project cost up to Rs. 40 crores (approximately $6 million). Till now, 74 such parks have been approved under the scheme.

- Not only that, but India’s manufacturing capabilities are also strongly backed by Government support through various schemes and incentives to make India globally competitive. The Government provides support in the form of export incentives and investment incentives. For the textile industry specifically, the Government has a scheme called the Amended Technological Upgradation Fund Scheme (ATUFS), under which capital subsidy is provided for acquiring benchmark machinery.

Various State Governments have also announced their textile and apparel policies aimed at attracting investments. One such lucrative policy that was announced by Gujarat in October 2017 is Gujarat’s Garment and Apparel Policy (GGAP). The policy aims to create 100,000 new jobs, thereby generating additional exports and attracting investment in the apparel sector over the next five years. Any enterprise with at least 150 new machines (Cutting & Sewing) with a minimum of 300 employees can avail incentives up to 125-130 per cent of the total capital investment over a period of five years.

- India also has an abundant human resource, in the form of skilled and English-speaking manpower. It is estimated that nearly 250 million people may enter the Indian workforce by 2030. English is the second most important language that is understood and is used commonly as a medium of spoken and written communication. This is another key advantage for global companies to set up their operations in India, whether sourcing or manufacturing. With an increasing emphasis on quality, the demand for skilled labour will rise in the coming years. Realizing this, the Government has implemented several initiatives to develop the pool of skilled manpower in India like Samarth (Scheme for Capacity Building in Textile Sector) that targets to train one million people over a period of three years (2017-20) with a budget outlay of Rs. 1,300 crores (approximately $190 million).

- The Indian textile industry is marked by the presence of large-scale manufacturers across the value chain, i.e., from yarn to finished goods. Many of these companies are already in partnerships or JVs with global companies. These diversified textile conglomerates have huge manufacturing capacities, compliant set-ups for high quality goods manufacturing and are well-recognized by world-wide buyers. In FY18, 49 listed Indian textile and apparel companies recorded an annual turnover of more than $100 million. There are many more opportunities in the Indian textile value chain which can be explored and that investors can reap benefit from, in different forms of partnership.

With the growing textile and apparel market of India and improving export competitiveness, there are significant opportunities across all fiber types and products. The market growth would not only increase demand for conventional products, but changing demographics and lifestyle would spur growth of several product categories which would involve categories like technical textiles, synthetic fabrics, intimate wear, women’s western wear and sportswear.

The Indian Government is also taking proactive steps to make the business environment in India conducive for local and foreign investors. India is a promising destination for FDI in the textile sector where 100% FDI is allowed under the Automatic Route. This means that foreign companies need not take any advance permission from the Indian Government related to FDI. They may initiate the process and inform the relevant authorities later on. In addition, the Ministry of Textiles has also set up a dedicated FDI cell to guide textile investors regarding investment in India.

We, at Wazir, believe that the opportunities are endless. However, an investor needs to maintain all checks and balances to establish a successful set-up. The key factors that will determine the success rate for any investment in the Indian textile sector include a mix of selecting the right opportunity, the right location, and a thorough understanding of consumer and operations. Evaluating a right opportunity also entails assessing internal and external competition, the business scale-up possibility, entry barriers, expected returns and the future sustainability of the business.

With decades of experience in the textile and apparel sector of the country, Wazir is one such catalyst that helps clients invest in India successfully by assisting them in strategy formulation, forming alliances and joint ventures, investments, market understanding, sector analysis and due diligence, thereby providing end-to-end solutions spanning the complete business cycle in the textile value chain. Wazir also provides complete implementation support to textile and apparel businesses.

All in all, the above trends indicate that the Indian economy, especially in the textiles & apparel sector, is booming. The country’s macro-economic stability, resilience to deal with external shocks and a stable political environment provide strong assurance for its spot as one of the most attractive global destinations for investments, and promise abundant growth at a healthy pace for all its stakeholders in the future as well.

By Varun Vaid, Associate Director, and Ayushi Puri, Consultant, Wazir Advisors

The author can be reached at varun@wazir.in